(All amounts in US$ unless otherwise specified)

VANCOUVER, British Columbia–(BUSINESS WIRE)–#CapstoneMining–Capstone Mining Corp. (“Capstone” or the “Company”) (TSX:CS) today announced production and financial results for the quarter (“Q4 2021”) and full year (“FY 2021”) ended December 31, 2021. Quarterly consolidated copper production totaled 51.6 million pounds at C1 cash costs1 of $1.72 per payable pound of copper produced. Annual consolidated copper production totaled 187.1 million pounds at C1 cash costs1 of $1.81 per payable pound of copper produced. Link HERE for Capstone’s Q4 2021 management’s discussion and analysis (“MD&A”) and financial statements and HERE for the webcast presentation.

Darren Pylot, CEO of Capstone, commented, “Our investments in optimization and expansion over the past two years have allowed us to take advantage of robust copper prices, positioning us now with a large net cash balance sheet ahead of a period of transformational growth.” Mr. Pylot continued, “We announced the upcoming business combination with Mantos Copper on November 30th. After the special meeting of the shareholders on February 28th, we look forward to building on the strengths of both organizations as we create Capstone Copper, a Canadian copper champion that will deliver leading growth in our sector. We remain committed to strengthening communities and building resilient long-life operations.”

Q4 2021 AND 2021 OPERATIONAL & FINANCIAL HIGHLIGHTS

- Record net income of $252.9 million, or $0.56 per share for 2021 and net income of $41.4 million, or $0.10 per share for Q4 2021. Adjusted net income1 of $241.6 million or $0.60 per share for 2021, and $73.2 million or $0.18 per share for Q4 2021; main reconciling item for Q4 2021 was share based compensation expense.

- Record Adjusted EBITDA1 of $432.2 million for 2021 and $113.3 million for Q4 2021. The increase in adjusted EBITDA1 is reflective of Capstone’s 19% growth in production and strong operational performance and financial leverage in a robust copper price environment.

- Record Operating cash flow before changes in working capital1 of $556.3 million in 2021 and $104.9 million in Q4 2021driven by strong revenue in a plus $4.40 price copper environment. Included in 2021 Operating cash flow is the receipt of the $150.0 million upfront payment for the Cozamin Silver Stream and $30.0 million upfront payment for the Santo Domingo Gold Stream Agreement.

- Cash and short term investments grew by $56.2 million during the three months ending December 31, 2021 and by $389.3 million during 2021 to $264.4 million. The Company’s total available liquidity1 was $489.4 million with nil long term debt. The balance sheet was further enhanced by continued strong operating cash flow generation during Q4 2021.

- Consolidated copper production of 51.6 million pounds at C1 cash costs1 of $1.72 per payable pound of copper produced for Q4 2021. Full year guidance achieved with consolidated copper production for 2021 of 187.1 million pounds at C1 cash costs1 of $1.81 per payable pound of copper produced.

- Cozamin Mine achieved another record quarterly copper production of 14.5 million pounds at $0.99 per payable pound of copper produced for Q4 2021. Q4 2021 production was 41% higher than in Q4 2020 following commissioning of the Calicanto one-way ramp in Q1 2021.

- Pinto Valley Mine produced 37.1 million pounds at $2.00 per payable pound of copper for Q4 2021. The mine’s processing plant achieved rates of approximately 58,500 tonnes per day (“tpd”) in Q4 2021 following completion of Phase 2 of PV3 Optimization.

- Capstone announced the Transaction to combine with Mantos Copper (Bermuda) Limited (“Mantos”) to create Capstone Copper Corp.The Transaction will establish Capstone Copper Corp. as a premier copper producer with a diversified portfolio of high-quality, long-life operating assets focused in the Americas with an extensive pipeline of near-term fully-permitted organic growth opportunities. Completion of the Transaction is expected in March or April 2022.

|

Operational Overview

Refer to Capstone’s Q4 2021 and FY 2021 MD&A and Financial Statements for detailed operating results.

Q4 2021 | Q4 2020 | FY 2021 | FY 2020 | |

Copper production (million pounds) | ||||

Pinto Valley | 37.1 | 34.1 | 133.3 | 119.0 |

Cozamin | 14.5 | 10.3 | 53.8 | 37.9 |

Total | 51.6 | 44.4 | 187.1 | 156.9 |

Copper sales | ||||

Copper sold (million pounds) | 46.8 | 39.3 | 178.7 | 147.4 |

Realized copper price ($/pound) | 4.61 | 3.64 | 4.42 | 2.99 |

C1 cash costs1 ($/pound) produced | ||||

Pinto Valley | 2.00 | 2.00 | 2.16 | 2.21 |

Cozamin | 0.99 | 0.63 | 0.96 | 0.69 |

Consolidated | 1.72 | 1.68 | 1.81 | 1.84 |

Consolidated

Q4 2021 production was 16% higher than Q4 2020 mainly as a result of higher mine grades at both mines plus record copper production at Cozamin driven by the mine expansion related to the completion of the new one-way ramp at the end of 2020.

2021 consolidated production of 187.1 million pounds of copper is at the upper end of the full year guidance of 175 to 190 million pounds of copper. The production results reflect a 19% increase compared to prior year, benefiting from Cozamin achieving the higher mill rates (3,800 tpd) and benefits of the PV3 Optimization projects at Pinto Valley. The increase in production was the main driver for the $0.03 per payable pound of copper decrease in C1 cash costs1 in 2021 compared to 2020, offset by $0.09/lb related to the Cozamin silver stream, thus overall pre-stream the C1 cash costs1 were $0.12/lb lower than 2020. 2021 YTD C1 cash costs1 are within annual guidance of $1.75 to $1.90 per payable pound of copper.

Pinto Valley Mine

Q4 2021 production was higher than the same period last year primarily on higher grades for Q4 2021 (0.37% versus 0.31% in Q4 2020) as a result of mine sequencing and an increase in cut off grade to the mill, sending the lower grade ore to leach, partially offset by lower recoveries in Q4 2021 compared to Q4 2020.

2021 production increased by 12% compared to the same period last year due to higher head grades for 2021 (0.35% versus 0.30% in 2020) and improved flotation plant recovery performance (85.7% versus 85.0% in 2020).

C1 cash costs1 of $2.00 per payable pound of copper in Q4 2021 were consistent with the same period last year. Lower capitalized stripping costs of $0.12 per pound during the quarter ($0.2 million versus $4.1 million in Q4 2020) were fully offset by higher Q4 2021 production compared to Q4 2020.

A decrease in 2021 C1 cash cost1 by $0.05 per payable pound of copper was primarily attributed to higher production compared to the same period last year.

Cozamin Mine

Production in Q4 2021 was 41% higher than the same period last year and another record production quarter for Cozamin. Higher copper production was primarily due to the successful utilization of the Calicanto one-way ramp which increased mill rates from 3,086 tpd in Q4 2020 to 3,863 tpd in Q4 2021. In addition, with the optimized technical report mine plan, the mine is delivering significantly higher mine grades (1.92% in Q4 2021 versus 1.72% in Q4 2020) from the copper rich San Jose and Calicanto zones.

2021 production increased by 42% compared to the same period last year mainly due to higher mill throughput (3,724 tpd versus 2,949 tpd in 2020 YTD) and head grades (1.86% versus 1.67% in 2020).

C1 cash costs1 in Q4 2021 were higher than the same period last year due to $0.29 per payable pound of copper impact of the Cozamin silver stream with Wheaton for 50% of the silver sales and higher production costs attributed to higher operating development meters executed.

C1 cash costs1 in 2021 were higher than the same period last year due to $0.30 per payable pound of copper impact of the Cozamin silver stream with Wheaton for 50% of the silver sales. The cost per payable pound impact of the Cozamin silver stream was partially offset by higher production.

Financial Overview

Refer to Capstone’s Q4 2021 and FY 2021 MD&A and Financial Statements for detailed financial results.

Q4 2021 | Q4 2020 | FY 2021 | FY 2020 | |

Revenue($ millions) | 215.9 | 148.1 | 794.8 | 453.8 |

Net income ($ millions) | 41.4 | 27.6 | 252.9 | 12.4 |

Net income attributable to shareholders ($ millions) | 41.4 | 27.6 | 226.8 | 12.6 |

Net income attributable to shareholders per common share – basic ($) | 0.10 | 0.07 | 0.56 | 0.03 |

Net income attributable to shareholders per common share – diluted ($) | 0.10 | 0.07 | 0.55 | 0.03 |

Adjusted net income1($ millions) | 73.2 | 35.6 | 241.6 | 26.4 |

Adjusted net income attributable to shareholders1($ millions) | 73.2 | 35.6 | 242.1 | 26.4 |

Adjusted net income attributable to shareholders per common share – basic1($) | 0.18 | 0.09 | 0.60 | 0.07 |

Adjusted net income attributable to shareholders per common share – diluted1($) | 0.18 | 0.09 | 0.58 | 0.07 |

Adjusted EBITDA1($ millions) | 113.3 | 63.5 | 432.2 | 139.2 |

Cash flow from operating activities2 ($ millions) | 94.5 | 67.4 | 553.3 | 147.2 |

Cash flow from operating activities per common share1 – basic ($) | 0.23 | 0.17 | 1.36 | 0.37 |

Operating cash flow before changes in working capital1,2 ($ millions) | 104.9 | 65.3 | 556.3 | 131.2 |

Operating cash flow before changes in working capital per common share1 – basic ($) | 0.26 | 0.16 | 1.37 | 0.33 |

2 2021 includes $180.0 million silver and gold stream proceeds |

December 31, 2021 | December 31, 2020 | |

Total assets ($ millions) | 1,728.0 | 1,391.6 |

Long term debt (excluding financing fees) ($ millions) | – | 184.9 |

Total non-current financial liabilities ($ millions) | 38.4 | 183.6 |

Total non-current liabilities ($ millions) | 481.3 | 408.5 |

Cash and cash equivalents and short-term investments ($ millions) | 264.4 | 60.0 |

Net cash/(debt)1 ($ millions) | 264.4 | (124.9) |

CORPORATE UPDATE

Mantos Transaction

On November 30, 2021, the Company announced it had entered into a definitive agreement (the “Agreement”) with Mantos to combine, pursuant to a plan of arrangement (the “Transaction”). Mantos is a copper-producing company that, through its subsidiaries, is engaged in the exploration, development, extraction, and processing of sulphide and oxide ores, and the production and sale of London Market Exchange Grade “A” copper cathodes and clean copper concentrates, with gold and silver by-products from its mining assets. Mantos Copper currently operates the open pit copper mines and processing plants of Mantos Blancos, located forty-five kilometers northeast of Antofagasta, and Mantoverde, located fifty kilometers southeast of Chañaral, in the region of Atacama.

The Transaction will require the approval of at least 66 2/3% of the votes cast by the shareholders of Capstone voting at a special meeting of shareholders to be held on February 28th, 2022. Officers and directors of Capstone, along with Capstone’s largest shareholder, have entered into support and voting agreements, agreeing to vote their shares in favour of the Transaction (representing approximately 26.5% of the issued and outstanding common shares of Capstone). The management information circular dated January 27th, 2022 has been posted to the Company’s website and filed on its profile on SEDAR.

Institutional Shareholder Services (“ISS”) and Glass Lewis (“GL”), two leading independent third party proxy advisory firms, have recommended that shareholders vote FOR the proposed business combination with Mantos. ISS and GL, among other services, provide proxy-voting recommendations to pension funds, investment managers, mutual funds and other institutional shareholders.

In its report, ISS stated, “The arrangement makes strategic sense as the combined company will possess a diversified collection of long-life operating assets, planned and fully financed copper production growth of 45% by 2024, and material production growth opportunities represented by the Santo Domingo project as well as expansion projects across the combined company asset portfolio.”

Glass Lewis’ report noted, “We ultimately believe the board and special committee established a sound basis upon which to conclude the proposed transaction represents an attractive opportunity for the Company and its shareholders. The merger will result in a larger, more diversified copper producer with an opportunity to achieve meaningful synergies.”

Upon completion of the Transaction, the combined company is expected to be renamed Capstone Copper Corp. (“Capstone Copper”). Capstone Copper will remain headquartered in Vancouver, B.C. and has received conditional approval to be listed on the TSX. Pursuant to the Agreement, each Capstone shareholder will receive 1 newly issued Capstone Copper share per Capstone share (the “Exchange Ratio”) and the existing Mantos shareholders will continue to hold Capstone Copper shares. Upon completion of the Transaction, former Capstone and Mantos shareholders will collectively own approximately 60.75% and 39.25% of Capstone Copper, respectively, on a fully-diluted basis. The Transaction is subject to certain regulatory approvals, consents from certain third parties and other customary closing conditions for a transaction of this nature, including approvals by the security holders, the TSX and the Supreme Court of British Columbia. The Agreement includes a non-solicitation provision, a right to match a superior proposal and a C$75 million termination fee payable in certain circumstances. Completion of the Transaction is expected in March or April 2022.

Subject to shareholder approval and the satisfaction of all other conditions, the Transaction is anticipated to close in March or April 2022.

PV3 Optimization Completed

PV3 Optimization work was completed in Q3 2021. The $31 million two year program involved investments in the fine crushing plant, two new ball mill shells, tailings thickeners, and tailings pumping upgrades. The optimization work has enabled the reliability of higher throughput rates at Pinto Valley from 51,000 tpd average in 2019 to over 58,000 tpd average in Q4 2021.

PV4 Study

During 2021, the study work progressed on the pre-feasibility study (“PFS”) for PV4 which aims to maximize the conversion of approximately one billion tonnes of mineral resources to mineral reserves, significantly extending Pinto Valley’s mine life and increasing the mine’s copper production profile. The application of the following new technologies and innovation is being considered:

- Expansion of the use of Jetti Catalytic Leach Technology which has the potential to increase mill cut-off-grades and increase tonnage available for leaching. Column leach testing is ongoing through H1 2022 and results will be included in the PV4 Study.

- Pyrite Agglomeration has strong Environmental, Social and Governance (“ESG”) implications as it will divert acid-generating minerals including pyrite and chalcopyrite from tailings to the dump leach operation. Additional copper recovery and lower costs via self–generation of free acid are also key economic drivers for this project. The project’s initiation is targeted for H2 2022 subject to board approval. Based on preliminary study results, the project is expected to require a low capex with a short payback period.

Higher mill throughput will be considered targeting up to 65,000 to 70,000 tpd. Key areas of investment include upgrades to ball mill motors, grinding circuit cyclones, and improvements to the rougher flotation circuit and evaluation of coarse particle flotation. A low capital strategy is currently under review to improve coarse particle recovery with some modest investment in the current conventional flotation circuit. An expanded dump leach strategy would translate to higher grades sent to the mill for processing and increased copper cathode production by expanding dump leach tonnage.

Santo Domingo Project

Following consolidation of Capstone’s 100% ownership of the Santo Domingo Project (“Santo Domingo” or “the Project”) in Region III, Chile during Q1 2021, the Company continued to advance the Project on several fronts:

- With respect to the reduced initial capital estimate, the Company and its port partner, Puerto Abierto, S.A., a subsidiary of Puerto Ventanas, S.A., are executing on early works in the framework agreement. In addition, the Company is advancing the analysis of the pipeline versus rail capital trade-off in which the proposals replace the pipeline capital to become a rail customer. This work is now being done in conjunction with the Mantoverde synergies analysis discussed below.

- With respect to the proposed Transaction with Mantos, scoping level work is being performed by the Santo Domingo and Mantos teams starting in late Q4 2021 to identify and refine potential synergies between the Santo Domingo Project with the Mantoverde mine (owned 70% by Mantos). Santo Domingo is situated ~35 kilometres northeast of the Mantoverde mine; significant potential opportunities exist for:

- Infrastructure sharing (including power, water, pipelines, port),

- Transportation synergies for concentrates,

- Potential enabling of product lines (additional iron and cobalt production from Mantoverde, processing oxide ore from Santo Domingo),

- Potential integrated operating approach, and

- Construction synergies (including project teams and camp).

- With respect to potential increases in the Chilean mining royalty tax, Santo Domingo is expected to be protected given the Company retains a foreign investment contract with the state of Chile, which fell under the provisions of DL600. One of the benefits to the Company of this agreement is a tax invariability system for a period of 15 years post commercial production.

- Cobalt Feasibility Update: The drilling program from Q3 and Q4 of 2021 generated sufficient sample mass for 2022 pilot scale testing of the cobalt recovery process. The first of a total of two stages of the cobalt feasibility engineering work, covering pre-feasibility level activities, started in September 2021 and is expected to finalize in March 2022. The proposed cobalt recovery process takes advantage of a tailings side-stream containing pyrite laden with ~0.6% cobalt, which will be recovered through a conventional flowsheet. The concentrate will be sent to pyrite roasting and solvent extraction followed by crystallization to produce battery grade cobalt sulphate heptahydrate. At an expected 10.4 million pounds of cobalt production per year, this will be one of the largest and lowest cost cobalt producers in the world at C1 cash costs1 of minus $4 per pound. Additional benefits of this project include the production of by-product sulphuric acid from the pyrite roasting process, which can be used for heap or dump leaching to produce low-cost copper cathodes at Santo Domingo, Mantoverde, and elsewhere in the district.

Corporate Exploration Update

Cozamin exploration: The focus during Q4 2021 was on testing the Mala Noche Footwall Zone and Mala Noche Main Vein West Target with three surface rigs, along with the in-parallel development of the west exploration drift and crosscuts which will allow more efficient testing of the target from underground once completed in early 2022. One additional surface rig tested other brownfield targets on the property.

Copper Cities, Arizona: On January 20, 2022, Capstone announced that it had entered into an 18-month access agreement with BHP Copper Inc. (“BHP”) to conduct drill and metallurgical test-work at BHP’s Copper Cities project (“Copper Cities”), located ~10 km east of the Pinto Valley Mine. In 2022, Capstone plans to spend $6.7 million in a two-phase drill program aimed at twinning historical drill holes and to select a portion of these for metallurgical testing.

Planalto, Brazil: Step-out drilling at the Planalto Iron Ore-Copper-Gold prospect in Brazil, under Earn In agreement with Lara Exploration Ltd., commenced in Q4 2021 and will continue into 2022. Lara Exploration Ltd. is expected to report results when appropriate.

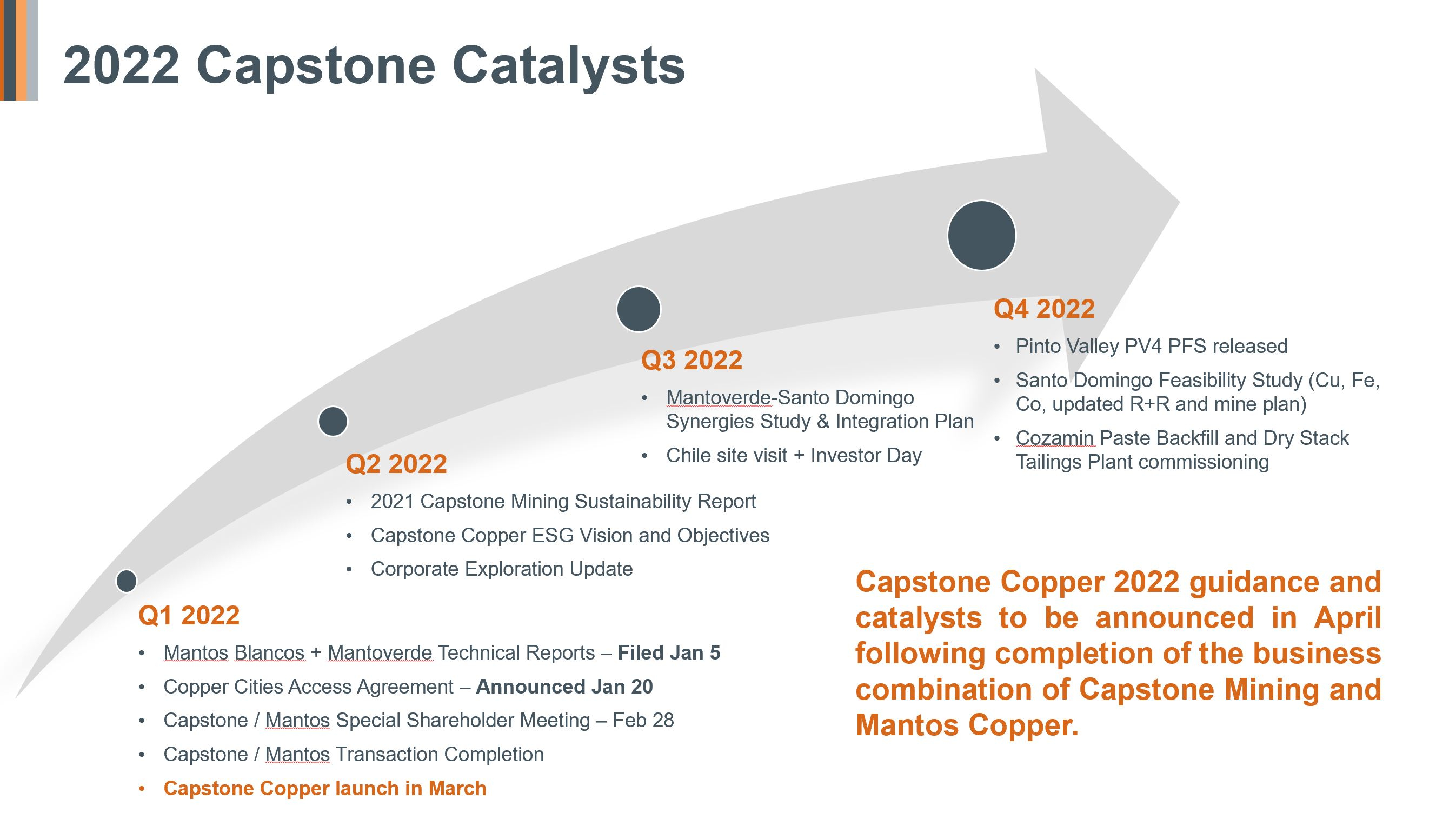

Capstone Copper 2022 Catalysts

The following chart demonstrates key catalysts this year and assumes the completion of the combination with Mantos Copper by the end of Q1 2022. Of note, Capstone Copper’s ESG Vision and Objectives will be rolled out in Q2 2022. The Mantoverde-Santo Domingo synergies study & integration plan is expected in September and will be followed by a site visit and investor day for institutional investors and analysts.

At Pinto Valley, the PV4 prefeasibility study is expected to be released by year-end and at Santo Domingo, the updated feasibility and mine plan including the cobalt feasibility study is also expected to be released in Q4 2022. At Cozamin, the paste backfill and dry stack tailings plant is expected to be commissioning by the end of 2022.

2022 PRODUCTION AND COST GUIDANCE

In 2022, Capstone Mining expects to produce between 82,000 and 90,000 tonnes of copper at C1 cash costs1 of between $1.85 and $2.00 per pound payable copper produced from the Pinto Valley and Cozamin mines.

Our cost control strategy included the following actions:

During 2020, financial hedges were executed on foreign exchange rates to protect approximately half of the Company’s Mexican Peso exposure from August 2020 through December 2021. The realized gain on the Mexican Peso zero cost collars was $2.6 million for the twelve months ended December 31, 2021. In November 2021, additional financial hedges were executed for approximate 75% of the Mexican Peso and Chilean Peso operating and capital cost exposure at the Cozamin mine and at Santo Domingo, respectively. The Mexican Peso collars have a floor of 20 and a cap of 24.75 Mexican Pesos to the US dollar, and the Chilean Peso collars have a floor of 750 and a cap of 931 and 939 Chilean Pesos to the US dollar.

Pinto Valley fixed diesel prices with a supplier on its expected 2021 and 2022 diesel consumption at $1.76/gallon and $2.13/gallon, respectively. The fixed diesel prices have resulted in cost savings of $3.0 million and $6.3 million during the three months and year ended December 31, 2021, respectively. At current prices the price fixing is expected to yield additional savings of approximately $4.5 million during 2022.

CONFERENCE CALL AND WEBCAST DETAILS

Capstone will host a conference call and webcast on Wednesday, February 16, 2022 at 08:30 am PT/11:30 am ET.

Link to the audio webcast:

https://produceredition.webcasts.com/starthere.jsp?ei=1524721&tp_key=1dedc36dcb

Dial-in numbers for the audio-only portion of the conference call are below. Due to an increase in call volume, please dial-in at least five minutes prior to the call to ensure placement into the conference line on time.

Toronto: (+1) 416-764-8650

Vancouver: (+1) 778-383-7413

North America toll free: 888-664-6383

Confirmation #50217755

A replay of the conference call will be available until March 2, 2022. Dial-in numbers for Toronto: (+1) 416-764-8677 and North American toll free: 888-390-0541. The replay code is 217755#. Following the replay, an audio file will be available on Capstone’s website at: https://capstonemining.com/investors/events-and-presentations/default.aspx.

This release is not suitable on a standalone basis for readers unfamiliar with Capstone and should be read in conjunction with the Company’s MD&A and Financial Statements for the three and twelve months ended December 31, 2021, which are available on Capstone’s website and on SEDAR, all of which have been reviewed and approved by Capstone’s Board of Directors.

ABOUT CAPSTONE MINING CORP.

On November 30, 2021, Capstone Mining and Mantos Copper announced that they have entered into a definitive agreement to combine pursuant to a plan of arrangement under the Business Corporations Act (British Columbia).

Contacts

Jerrold Annett, SVP, Strategy and Capital Markets

647-273-7351

[email protected]

Kettina Cordero, Director Investor Relations & Communications

604-262-9794

[email protected]